The three most prominent national market trends for residential real estate are the ongoing lack of abundant inventory, the steadily upward movement of home prices and year-over-year declines in home sales. Sales declines are a natural result of there being fewer homes for sale, but higher prices often indicate higher demand leading to competitive bidding. Markets are poised for increased supply, so there is hope that more sellers will take advantage of what appears to be a ready and willing buyer base.

Closed Sales increased 4.2 percent for existing homes and 18.1 percent for new homes. Pending Sales decreased 3.9 percent for existing homes but increased 5.9 percent for new homes. Inventory decreased 29.2 percent for existing homes but increased 4.2 percent for new homes. The Median Sales Price was up 6.1 percent to $173,000 for existing homes but decreased 1.2 percent to $325,500 for new homes. Days on Market decreased 15.6 percent for existing homes but increased 4.2 percent for new homes. Supply decreased 30.0 percent for existing homes and 3.6 percent for new homes.

In February, prevailing mortgage rates continued to rise. This has a notable impact on housing affordability and can leave consumers choosing between higher payments or lower-priced homes. According to the Mortgage Bankers Association, the average rate for 30-year fixed-rate mortgages with a 20 percent down payment that qualify for backing by Fannie Mae and Freddie Mac rose to its highest level since January 2014. A 4.5 or 4.6 percent rate might not seem high to those with extensive real estate experience, but it is newly high for many potential first-time home buyers. Upward rate pressure is likely to continue as long as the economy fares well.

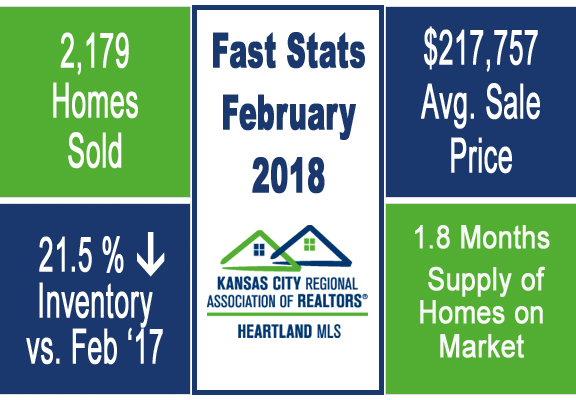

For more specific market numbers, click here.

*Information provided courtesy of KCRAR and Heartland MLS