The average 30-year fixed rate mortgage exceeded 5% in April, the highest level since 2011, according to Freddie Mac.* The recent surge in mortgage rates has reduced the pool of eligible buyers and has caused mortgage applications to decline, with a significant impact on refinance applications, which are down more than 70% compared to this time last year. As the rising costs of homeownership force many Americans to adjust their budgets, an increasing number of buyers are hoping to help offset the costs by moving from bigger, more expensive cities to smaller areas that offer a more affordable cost of living.

Closed Sales decreased 7.3 percent for existing homes and 10.1 percent for new homes. Pending Sales decreased 0.5 percent for existing homes and 21.4 percent for new homes. Inventory decreased 23.2 percent for existing homes but increased 27.8 percent for new homes. The Median Sales Price was up 13.1 percent to $273,750 for existing homes and 13.6 percent to $484,997 for new homes. Days on Market decreased 15.8 percent for existing homes and 23.9 percent for new homes. Supply decreased 30.0 percent for existing homes but increased 61.1 percent for new homes.

Affordability challenges are limiting buying activity, and early signs suggest competition for homes may be cooling somewhat. Nationally, existing home sales are down 2.7% as of last measure, while pending sales dropped 1.2%, marking 5 straight months of under contract declines, according to the National Association of REALTORS®. Inventory remains low, with only 2 months supply at present, and home prices continue to rise, with the median existing home at $373,500, a 15% increase from this time last year. Homes are still selling quickly, however, and multiple offers are common in many markets.

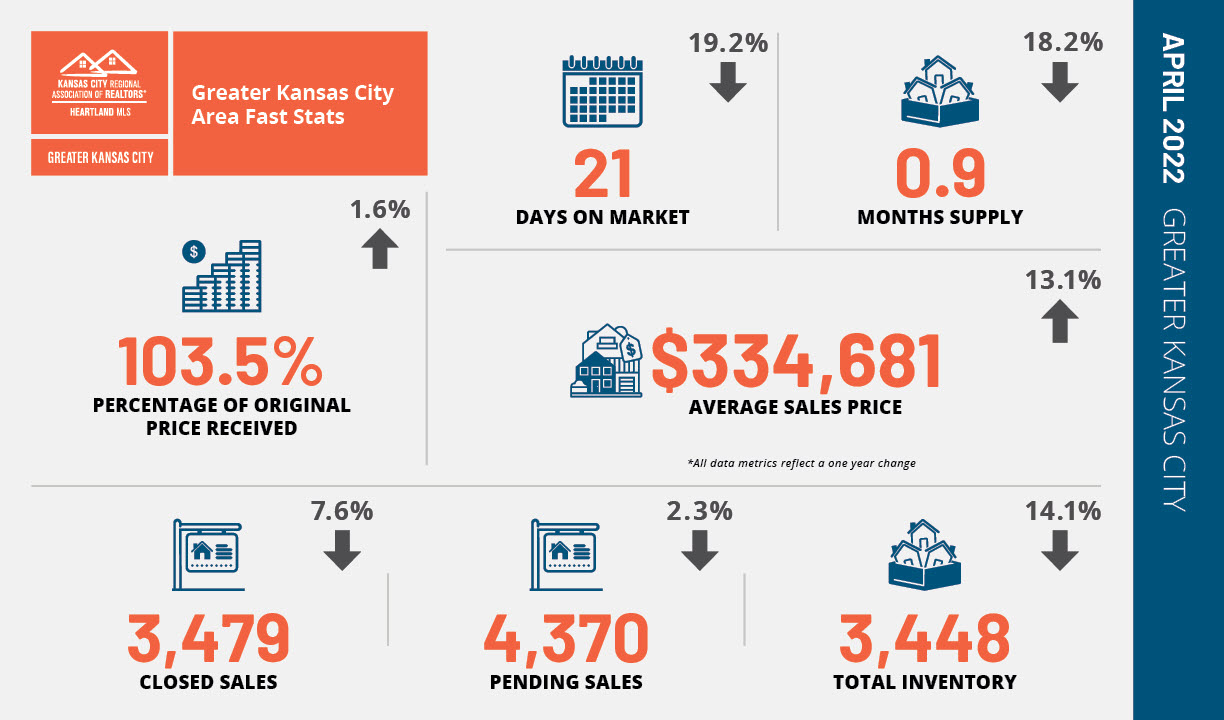

*Information and stats courtesy of KCRAR and Heartland MLS.